The Rule of 72: Learn How To Double Your Money with Compound Interest

Did I have you at "double your money"?

The Rule of 72 is one of the first tools I reach for when evaluating a company. It is fast, it is simple, and it tells me something important right away: how long it will take an investment to double at a given rate of return.

Most people treat it as a classroom concept. I use it in real time, in my head, while I am looking at actual businesses. That is what makes this page different from every other Rule of 72 article you will find.

If you have listened to InvestED or read either of my books, you have seen me reach for this formula more than once. It is simple to learn and easy to use, and it is one of the most useful tools any Rule #1 investor can have.

But most people searching for the Rule of 72 are really asking a bigger question: am I actually on track to build real wealth? That is what this article is about. The formula, how to use it, and what it takes to make the numbers work in your favor.

What Is the Rule of 72?

The Rule of 72 is a simple equation for calculating investment doubling time. Divide 72 by your annual rate of return and you get an instant estimate of how long your money takes to double.

It's a shortcut that you, as an investor, can use to estimate if an investment will double your money quickly enough to be worth pursuing. When you see how quickly your money can double, you'll understand the power of compound interest doubling your wealth over time.

What Is Compound Interest?

Compound interest is the engine behind how to double your money. The longer your money is invested, the faster it grows. The Rule of 72 applies to cases of compound interest, not simple interest.

The difference matters: with simple interest, you only earn a return on your original principal. With compound interest, your earnings get added back to your investment and start earning returns themselves.

That said, if your money is sitting in a low-yield savings account earning 0.5%, the Rule of 72 formula tells you it would take roughly 144 years to double. Compounding only works as hard as the annual rate of return behind it. That's why understanding the difference between saving vs investing matters.

Why Does the Rule of 72 Matter for Rule #1 Investors?

Investing well is about making smart, informed decisions, not gambling with your future. The Rule of 72 helps you set realistic expectations and spot opportunities or red flags before you commit capital.

For example, if someone promises you a "guaranteed" 24% return, the Rule of 72 tells you your money would double in just three years (72 ÷ 24 = 3). That's a huge red flag. If it sounds too good to be true, it probably is. Use this rule to keep your feet on the ground and your goals in sight.

How I Use the Rule of 72 to Value a Business

Here's something most investors don't realize: I use the Rule of 72 directly inside my Sticker Price calculation, the price I'm actually willing to pay for a business.

Here's how it works, for illustrative purposes only:

My minimum acceptable rate of return is 15%

At 15%, the Rule of 72 tells me money doubles every five years (72 ÷ 15 ≈ 5)

Over a 10-year holding period, that's two doubles

Two doubles means the Sticker Price today is roughly one-quarter of the Future Market Price

Example: if a business will be worth $320 per share in 10 years, the Sticker Price today is $80 ($320 ÷ 4 = $80)

And I never pay the Sticker Price. I always want a Margin of Safety, because no matter how solid my analysis is, things don't always go exactly as planned. That means buying at 50% off Sticker. In this example, that's $40.

Use the Margin of Safety calculator to run this on any company you're researching. I use this calculation on every company I look at. It takes about 30 seconds.

How to Use The Rule of 72 Formula

The double investment formula works like this: divide 72 by your annual rate of return.

72 ÷ annual rate of return = number of years required for your money to double

Trying to compute what interest rate you'll need to double your money, given a specific number of years? Use this modified version instead:

72 ÷ number of years = required annual rate of return

Here's an example, for illustrative purposes only.

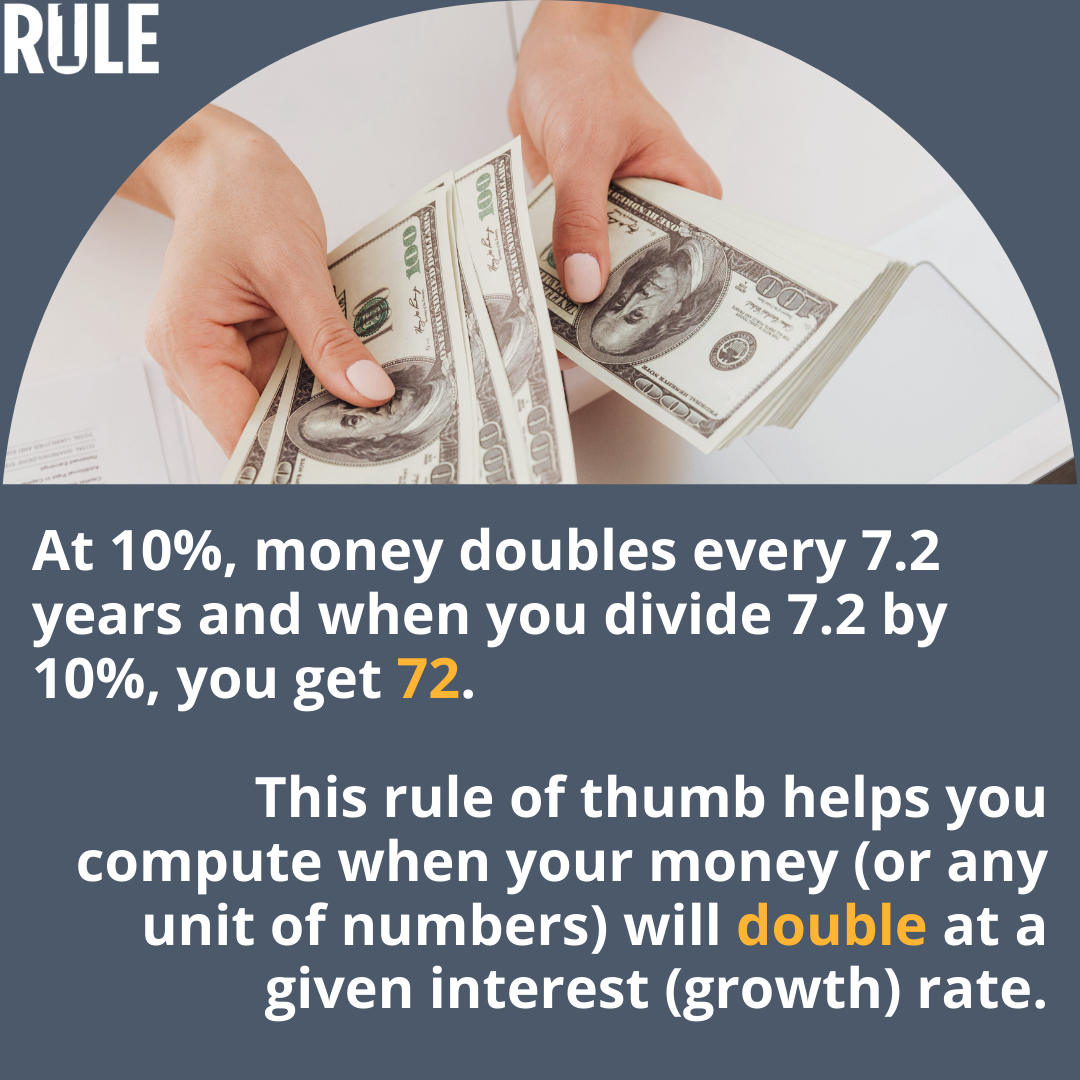

If you're earning a 10% annual rate of return, your money will double in approximately 7.2 years (72 ÷ 10 = 7.2). This is an approximate number, but it is an incredibly useful estimation tool for quick financial planning.

For more complex equations related to evaluating your investments, use these investment calculators to crunch the numbers.

Examples of the Rule of 72

Here are a few rule of 72 examples to make the formula concrete.

Given a 9% interest rate, how long will it take to double your money? Divide 72 by 9 and you'll get 8 years.

Now let's apply this to a scenario where you already know the number of years you need to double your money, and you need to work out the required rate of return. You just need to reverse the equation.

Say you want to double your money in 3 years so you can put a down payment on a house.

Divide 72 by 3 to get 24. You will need a 24% rate of return on your investment. If you later decide not to buy the house and instead leave your money invested for another 6-7 years, it would double two more times.

If you started with $10,000, then after three years you would have $20,000. After another three years, you would have $40,000, and after another three years, you would have $80,000. That's eight times your starting amount, and it only took nine years, given a 24% annual rate of return.

That is the power of compound interest, and exactly what makes investing such an incredible way to grow your wealth over time

Drawbacks of the Rule of 72

The Rule of 72 is an estimation; it's not exact.

Take the example above. At a 24% growth rate, the exact doubling time is 3.2 years, not 3.

It's most accurate with annual compounding and fixed annual rates around 10%. The further you get from that, the less precise the estimate becomes.

The Rule of 72 assumes a fixed annual rate and doesn't account for market volatility, fees, or costs. Past performance doesn't guarantee future results. Always use it as a ballpark estimate, not a guarantee.

Here's the real limitation: the formula assumes your returns are consistent year over year. In reality, they're not.

Say you have $10,000 invested and you lose 50% in a rough year. You're now at $5,000. To get back to $10,000, you don't need a 50% gain. You need a 100% gain. And how long that recovery takes depends entirely on your annual rate of return:

At 10%, the Rule of 72 tells you recovery takes roughly 7 years

At 15%, it takes about 5 years

At 26%, you're back in under 3 years

That gap is the difference between a detour and a decade lost.

That's not a disclaimer. That's math. That's why I evaluate before I buy. I want to know what return I can reasonably expect, not hope for.

To do that, I use the Four M's: Meaning, Moat, Management, and Margin of Safety.

When to Use the Rule of 72

The Rule of 72 is useful any time you need a fast estimate: planning for retirement, evaluating an investment, or understanding the real cost of debt.

To Plan for Financial Goals

Start with a specific goal. The Rule of 72 will tell you exactly what return you need to get there.

Two examples:

Starting with $50,000, needing $100,000 in 10 years:

You need a 7.2% annual return (72 ÷ 10 = 7.2%)

Starting with $15,000, needing $100,000 in 10 years:

You need your money to double roughly 3 times, or every 3.3 years, which requires a 21.8% annual return (72 ÷ 3.3 = 21.8%)

If you are investing for retirement, the Rule of 72 can be extremely beneficial. The amount of money you will need for retirement is a big number, but if you start early, even a small amount of money can double over and over again. Use ourretirement calculator to see how many doublings you can realistically target before youretire early.

The less time you have until retirement, the higher the return you need. The more time you have, the more flexibility you have on rate.

To Evaluate Investments

Of course, this is how I use it most.

Take two investments side by side:

Investment A at 18%: doubles every 4 years (72 ÷ 18 = 4)

Investment B at 14%: doubles every 5.1 years (72 ÷ 14 = 5.1)

Over 15 years: Investment A doubles nearly 4 times. Investment B doubles roughly 3 times.

That's nearly an extra doubling from a 4% difference in return.

Here's what that gap looks like over 20 years, starting with $10,000.

(For illustrative purposes only. Actual results will vary.)

Same starting amount. Same 20 years. A $1,120,000 difference between the lowest and highest return.

To Better Understand Debt and Inflation

The formula works the same whether it's working for you or against you.

On the debt side:

At 20% credit card interest: balance doubles in 3.6 years if unpaid (72 ÷ 20 = 3.6)

At 24% interest: doubles in just 3 years (72 ÷ 24 = 3)

On the inflation side:

At 3% average inflation: purchasing power halves in 24 years (72 ÷ 3 = 24)

A dollar saved today in a low-yield account may only buy half as much in 24 years

That is not a dramatic crash. It is a slow, quiet erosion.

Understanding inflation and your money is the first step toward doing something about it.

How To Double Your Money

Let's say hypothetically that we're aiming for a 26% annual return as a benchmark, purely for illustrative purposes. At that rate, the Rule of 72 tells us money can double roughly every three years (72 ÷ 26 = 3).

Why 26%? The rationale is in the methodology. When you buy a wonderful business at a significant discount to its true value, the return potential is already built into the price before the business grows a single dollar.

Warren Buffett has averaged around 20%+ for decades by buying wonderful businesses at attractive prices. Aiming slightly higher simply accounts for the uncertainty in any analysis.

Getting there takes financial education, patience, and the discipline to evaluate companies before you buy.

The Four M's: How I Find Returns Worth Doubling

Here's the process I use to find companies worth running through the Rule of 72.

Meaning: I only invest in businesses I understand well enough to predict their future. If I can't explain what they do and why they'll still be doing it in 10 years, I move on.

Moat: A durable competitive advantage means more predictable growth, and that's what makes a return target meaningful rather than hopeful. I look at the

to confirm the moat exists: ROIC, sales, EPS, equity, and free cash flow, all growing at 10% or more per year for the last 10 years.

Management: Honest, owner-oriented leaders protect the business and its long-term compounding potential. I want people running the company who think like owners.

Margin of Safety: I never pay the Sticker Price. Buying at 50% off means the return advantage is structurally built in before the business grows a dollar.

Learn how to apply the Four Ms of Rule #1 Investing to real companies at the Virtual Investing Workshop, where I walk through every step live.

Common Questions About the Rule of 72

What is the Rule of 72 formula?

Simple. Divide 72 by your annual rate of return to estimate how many years it takes your money to double. If you want to work backwards, figuring out what return you need to double in a set number of years, divide 72 by the number of years instead. How long does it take to double your money?

It depends on your rate of return. At 10%, the Rule of 72 tells you it takes roughly 7 years. At 26%, just under 3 years. The higher your annual return, the faster your money doubles.

What is investment doubling time?

Investment doubling time is how long it takes your money to double at a given rate of return. The Rule of 72 gives you a fast estimate: divide 72 by your annual return and you have your answer in seconds.

Why does the Rule of 72 use 72 and not 70 or 69?

Divisibility. 72 divides evenly by 2, 3, 4, 6, 8, 9, and 12, which covers most common interest rates and makes the mental math simple. If you want more precision, 69.3 is the mathematically exact constant for continuous compounding. And 70 is commonly used in economics for GDP and inflation models. For everyday investing with annual compounding, 72 is the most practical choice.

How accurate is the Rule of 72?

Most accurate when rates are around 10% with annual compounding. The further you move from that, the more the estimate drifts. At a 24% growth rate, for example, the exact doubling time is 3.2 years, the Rule of 72 gives you 3. Close enough for most decisions, but not something to build a precise financial plan around.

What is the most precise way to calculate doubling time?

The exact formula is: Doubling time = ln(2) ÷ ln(1 + r), where r is your annual return as a decimal. At 9%, that gives you 8.04 years. The Rule of 72 gives you 8. For most investing decisions, the approximation is close enough.

What return do I need to double my money in 10 years?

7.2%. Just reverse the formula: 72 ÷ 10 = 7.2. That's the annual rate of return you'd need to double your money in a decade.

How is the Rule of 72 used in retirement planning?

It helps you estimate how many times your savings can double before you retire. The earlier you start, the more doublings you can expect; even at a modest return. If you're starting late, the Rule of 72 quickly shows you how much harder your money needs to work. Use our retirement calculator to model your own timeline.

Is the Rule of 72 just for stocks?

Nope. You can use it for any investment or debt with a fixed compound rate, bonds, mutual funds**, savings accounts, even credit card debt. The formula works the same regardless of the vehicle.**

Does it work for inflation, too?

Absolutely. If inflation is 3%, your purchasing power halves in 24 years (72 ÷ 3 = 24). That’s a sobering thought for any financial planning.

What about taxes?

Taxes reduce your effective rate of return, which extends your actual doubling time. If you earn 10% but taxes bring your effective rate down to 8%, the Rule of 72 tells you doubling takes 9 years instead of 7.2. Always factor taxes in for a more accurate picture.

Does the Rule of 72 work differently inside a 401k or IRA?

Yes, and in your favor. Inside a tax-advantaged account, your returns compound without taxes taking a cut each year. That is exactly what the Rule of 72 assumes. Outside those accounts, taxes reduce your effective rate and slow your doubling timeline.

That said, the account is just the vehicle. What you put inside it determines your return. A 401k full of mediocre mutual funds still compounds slowly.

Final Thoughts on The Rule of 72

The formula is simple. What matters is the return you plug into it, and that comes from knowing how to find and value wonderful businesses. If you are just getting started, how to invest money is a good next step.

When you're ready to go deeper, join me at the Virtual Investing Workshop. That's where I teach the full process live.

Editor's Note (Updated 2026): This article was originally published in 2021 and has been significantly updated in 2026 to reflect current examples and Rule #1 investing insights.